This article is more than 1 year old

Juniper pushes up sales and profits in Q1

Data center switches, service provider routers start to pick up

The top brass at Juniper Networks are breathing a little bit easier as the company turned in numbers that show it is growing despite taking a big hit in sales of gear, software, and services to the US government in the first quarter.

In the quarter ended in March, Juniper nudged up revenues by 2.6 per cent to $1.03bn, and net income shot up by a factor of 5.6 to $91m, showing that the restructuring that it did back in October, where it cut its workforce by 5.3 percent, is starting to show positive effects. (Well, except for the people who were shown the door.)

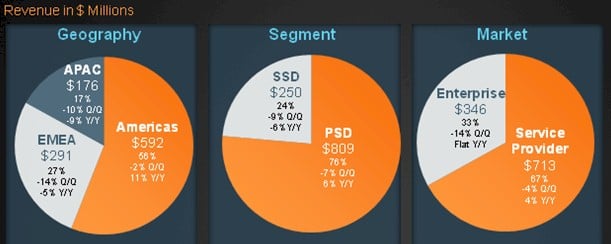

Hardware and software product sales increased by only 1.3 per cent in Q1, to $781.8m, while services revenues in the quarter jumped 6.5 per cent to $277.4m. It is still tough slogging out there in Network Land. And particularly so for Juniper in this quarter for its security software products, which fell 18.7 per cent to $136.7m.

That security software is tucked up inside of the Software Solutions Division, a new segment that Juniper created last year to carve out some of its software from its core switching and routing business. This segment also includes a smidgen of routing software not tied directly to its MX and PTX series of products, and that accounting for $25.5m in revenues in the quarter, up 12.8 per cent.

Services for SSD software products brought in $87.8m, an increase of 15.5 per cent over the year-ago period. Add them up and the SSD segment had $250m in sales, down 6.3 per cent. This was not the kind of number that Juniper was expecting to show for its fledgling standalone software biz or it would not have carved it out in the first place.

The Platform Systems Division, which peddles switches and routers and the software that is tied very closely to that iron, accounted for $809.2m in sales in the first quarter, up 5.7 per cent. Routing product sales were up 6.7 per cent to $488.1m, and switching products were up by 6.5 per cent to $131.5m.

Europe and Asia presented some difficulties for Juniper in Q1

In a conference call with Wall Street analysts after the markets closed on Tuesday, Kevin Johnson, CEO at Juniper, said that sales to service providers grew for the third quarter in a row and that router sales in the United States were strengthening, as Juniper had been expecting.

And, as it turns out, two customers – AT&T and Verizon – each generated 10 per cent of the company's sales in the quarter across all product lines. The service provider segment accounted for $712.9m in revenues, up 4 per cent.

Juniper has just announced 100Gb/sec line cards for its MX2020 edge routers, which are starting to ramp, and the PTX Series supercore routers and T4000 core routers are ramping as well now. (Router sales were down for the 2012 year, so this is a big deal for Juniper.)

Robyn Denholm, CFO at Juniper, said in the call that sales at US-based carriers, cable companies, and content providers was up 18 per cent, year-on-year.

But the enterprise space, where Juniper is selling into corporate rather than service provider and telco data centers, had flat performance thanks in large part to a 25 per cent dive in spending by the US government in the first quarter.

All told, Juniper's sales to enterprises was down two-tenths of a point to $346.3m. But, the QFabric line of modular switches is gaining traction, according to Johnson, and the company has just launched its EX9200 programmable switches, which should help keep things chugging along for the remainder of the year.

Looking ahead to the second quarter, Denholm said that Juniper expected sales of between $1.07bn and $1.10bn, against sales of $1.074bn in Q2 2012. Non-GAAP earnings per share were 19 cents in Q2 2012, and Juniper is projecting non-GAAP EPS to be between 22 and 26 cents in Q2 2013.

So revenues are basically flat to up a smidgen, but profits could rise 16 to 37 per cent on a non-GAAP basis. That is better than a kick in the ASICs. ®